AUTO INSURANCE

Auto insurance is a critical financial safeguard that protects you in the event of an accident, theft, or other unexpected disaster. But this protection comes at a cost, and it’s different for everyone. The car insurance industry uses information about what kind of car you have, how you drive, and who you are (your age, marital status, even your credit score) to help determine your risk and your rate. Insurance also varies substantially by location because each state has its own insurance requirements and regulations. And with hundreds of insurance companies in the U.S. using a mix of some 43,500 rating factors, any given driver could potentially choose from hundreds or thousands of quotes.

sTATE OF aUTO INSURANCE

Down for the first time since 2013

The average care insurance rate fell 4% from 2020

to 2021. The rates last feel in 2013 by 6.3% and typically drop when customers file fewer and/or less expensive claims. Even though the rates dropped this year, they’ve increased 24%, or $289 on average, since 2011.Cost is different everywhere

The cost of care insurance, and the impact of rising rates, is significantly different from one place to the next. Since 2011, rates have increased (as much of 80%) in 43 states and Washington, DC, while six states saw rate decreases of up to 20% and one state – Delaware – stayed the same. Since last year, rates have changed as much as 18% in some states.Rates were affected by COVID-19

As COVID-19 created unprecedented changes to typical travel habits, the number of miles traveled by US drivers dropped 14% from 2019-2020, according to the Federal Highway Administration. Insurers offered rebates and reduced rates as the pandemic took full effect, returning $14 billion to customers. The fewer miles someone drives, the less their insurance costs. Typically, the savings are small – about 3.6% - but drivers in some states can save up to 32% by reducing their annual mileage.

WHY ARE RATES CHANGING

When risks change, rate reflect that change and insurance is all about risk. Car insurance pricing considers individual risks associated with drivers and their vehicles, but broader environmental, government and economic factors also play a role.

WEATHER

Wildfires, flooding, hurricanes, hailstorms – catastrophes like this cause widespread property damage and an onslaught of insurance claims in a given area. Insurance companies raise rates to account for these losses. In 2020, the US saw higher numbers of wildfire, hurricanes and tropical storms, and fewer – but deadlier – tornadoes than in 2019. Together, these natural catastrophes accounted for tens of billions of dollars in insured property losses, according to industry analysis.

POPULATION AND CRIME

Even thought drivers were legally required to have auto insurance virtually everywhere in the US, more than 13% of Americans are driving uninsured. More populated cities and those with more traffic congestion, crime and uninsured drivers often have higher insurance rates. The US population is up more than 6% since 2011, and top metro areas are growing even faster. More than 721,000 vehicles were stolen in the US in 2019. This represents a 4% decrease from 2018, but a 5.1% increase compared to 2014.

ECONOMY AND BEHAVIOR

Americans are increasingly distracted by phones and other devices behind the wheel. This and other reckless behaviors (like aggressive driving and DUI) increased risk, therefore increase rates for everyone. Even with fewer people on the road, distracted driving is dangerous. Early studies show that crashes were 14% more fatal for single-care accident and 59% more fatal for multi-car accidents in 2020 than they were in 2019.

As roads cleared during lockdowns, people started speeding more, leading to speeding tickets and dangerous accidents. Insurers’ data shows that drivers with a history for traffic violations and accidents tend to file more claims than those who don’t, so they raise those drivers’ insurance rates accordingly.

LEGISLATION AND REGULATION

Each state has its own insurance laws and government regulators. Each sets a minimum level of coverage residents must carry, determines if and when insurance companies can raise rates, and proposes new laws regarding fraud and more.

Insurance departments in some states have prohibited certain factors from being used to price insurance – notably genre, credit score and level of education – arguing that they are discriminatory and irrelevant to a driving risk. In 2020, Michigan became the newest state, alongside California, Hawaii and Massachusetts, to ban these personal rating factors. As of late 2020, Congress is considering a bill that would ban personal rating factors like gender, credit, zip code and income nationwide.

CAR INSURANCE RATES IN THE US

Rates by AREA

In the past year, car insurance rates fell in 33 states and rose in 17 states and Washington, D.C. Maine saw the biggest year over year rate increase at 18%, while Michigan had the biggest decrease at -18%. However, Michigan still leads as the most expensive state for car insurance, and Ohio trails as the least expensive.

Rates by Age

Car insurance companies closely relate a driver’s age to their level of experience. Young, inexperienced drivers are more likely to get in an accident than older drivers, so young drivers pay higher rates.

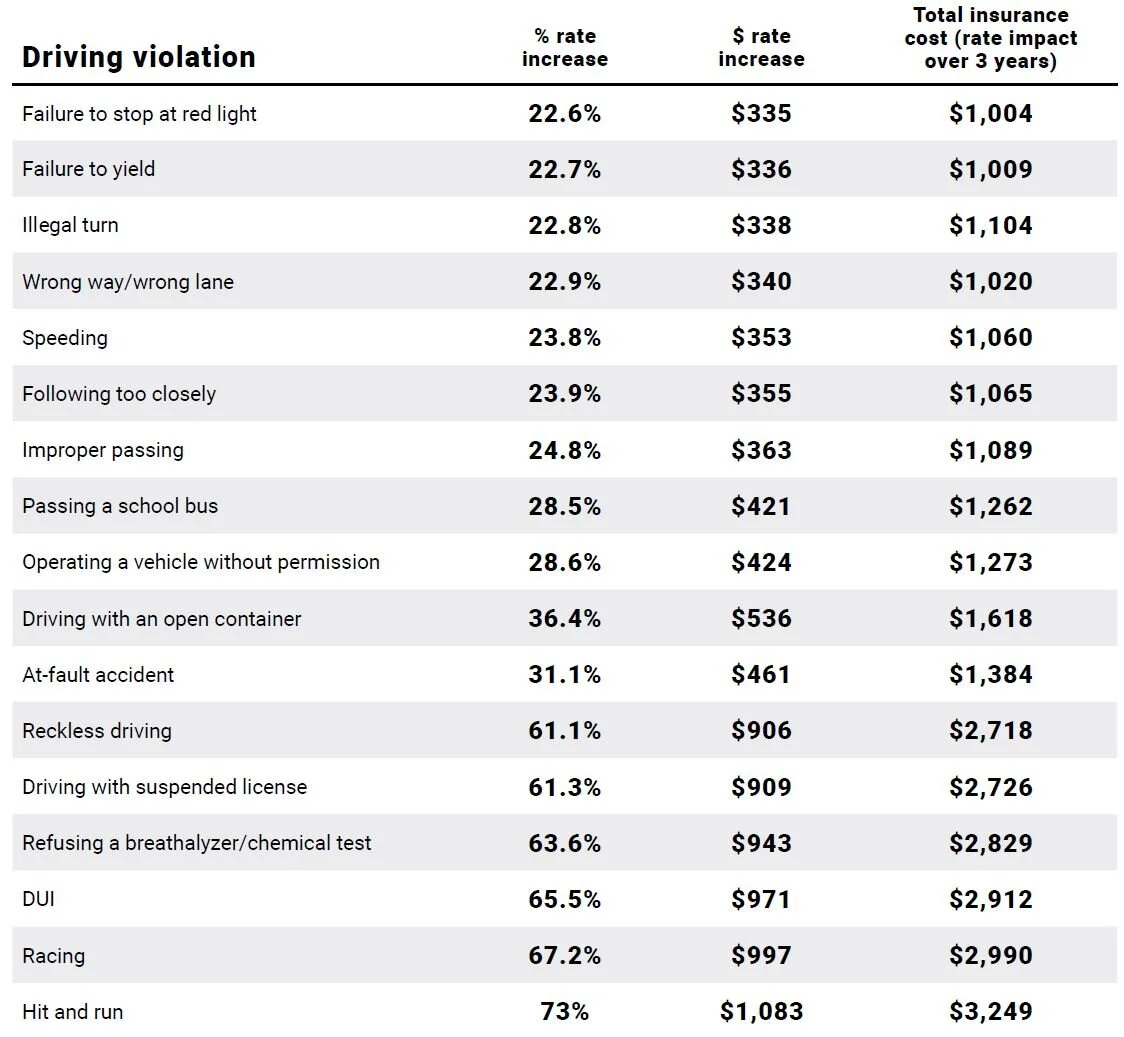

how your driving record affects your insurance

Your driving record significantly impacts what you pay for car insurance, and some violations and claims are much more costly than others. Insurers in all states can factor these violations into your car insurance rate for three years — or longer.

Annual mileage & primary use

Your annual mileage usually has little impact on car insurance rates – unless you live in California. Nationally, drivers save about 6% by reducing their driving from 15,000 miles per year to less than 7,500 miles per year. Californians, however, would save 32%, or $549, for halving their mileage. Typically, the average American drives about 12,000 miles per year. Of course, in 2020 that changed. The total mileage across America was down 14% compared to 2019.

The majority of drivers have personal-use policies, meaning they use their car for a mix of commuting to work, running errands and other personal tasks. However, some drivers need a different type of coverage. People who drive for business — such as real estate agents or traveling salespeople — need a policy that covers them when using their car for work. Driving for pleasure usually means you have multiple cars and one is more for weekend cruising, while farm-use vehicles require a limited, special license.

how much coverage do you need?

Liability coverage is required (it’s the law), but you’ll need to add comprehensive, collision and other coverages if you want to protect your vehicle and yourself. Many drivers also opt to increase liability coverage above the state required minimum to safeguard against the most serious and costly accidents. State minimum liability coverage offers the least amount of protection for the lowest price. Policies that add comprehensive and collision protect your vehicle against events like floods, hail, and crashes — but they cost twice as much. The deductible you select (typically $500 or $1,000) also affects your rates. The deductible is the amount you pay out of pocket for a claim before your insurance company pays anything.

Insurance coverage 101

Bodily Injury: 50 per person

Bodily Injury: 100 per accident

Property Damage: 50

These numbers represent the limits of how much your insurer will pay to cover injury and property damage costs after an accident. Each state has minimum liability requirements, but drivers may buy more coverage for extra protection. For example, 50/100/50 means you have coverage up to $50,000 for each person injured in an accident you cause, up to $100,000 for all people injured in the accident, and up to $50,000 for property damage. If you cause damage that exceeds these limits, you’re on your own to cover the rest.

Liability coverage

Liability cover pays for injuries and property damage suffered by other people when you’re at fault in an accident. This coverage is legally required for drivers everywhere in the U.S. (except New Hampshire) – but note that liability does not cover your own vehicle damage or injuries.

Property damage liability coverage is part of a car insurance policy that helps pay to repair damage you cause to another person's vehicle or property. This type if coverage is required by most states and typically helps cover the cost of repairs if you are at fault for a car accident that damages another vehicle or property such as a fence or building front.

If you cause a car accident that injures another person, bodily injury liability coverage helps pay for their medical expenses and lost income as a result of their injuries. This coverage may also help pay for your legal fees if you're taken to court over an accident. Most states have laws that require you to have bodily injury liability coverage on your car insurance policy.

COLLISION COVERAGE

Collision insurance is a coverage that helps pay to repair or replace your car if it's damaged in an accident with another vehicle or object, such as a fence or a tree.

Collision coverage pays for damage to your vehicle if it hits another car or inanimate object, whether its a minor fender-bender or major highway pileup.

If you're leasing or financing your car, collision coverage is typically required by the lender. If your car is paid off, collision is an optional coverage on your car insurance policy.

Collision insurance does not cover damage to your vehicle not related to driving (examples: hail or theft), damage to another person's vehicle, medical bills (yours or another person's).

Collision coverage has a deductible, which is the amount you pay before your coverage helps pay for your claim. You can typically choose the amount of your collision deductible when you buy coverage. Depending on your insurer, you may have several deductible amounts to choose from -- typically $0, $500 or $1,000.

If you choose a lower deductible, your premium will likely increase. Likewise, If you choose a higher deductible, your premium may decrease. Keep in mind, however, you will have to pay your deductible out of pocket toward car repairs as part of a covered claim.

Comprehensive coverage

Comprehensive covers damage to your vehicle in all kinds of unexpected scenarios that aren’t accidents with other cars. This includes (but is not limited to) weather damage and theft. You may also see this written as “other than collision” coverage.

HOMEOWNER INSURANCE

It's not uncommon to find out at the end of your policy term that your home insurance rates are going up. The amount you pay in premiums is largely dependent on your home’s location, the age of your home, and your insurance score — so if any of the factors that affect your premiums have changed, that might explain your rate increase.

Rates may also be affected by factors that are completely out of your control, like changes in the insurance industry. When carriers suffer a record-setting number of losses in a given year, that affects the industry’s bottom line, and there’s a good chance the following year’s rates will reflect that — often at the behest of reinsurance companies.

Earlier this year more than 50,000 Floridians lost their home insurance, and many were unaware it was going to happen. The three insurance companies that dropped more than 50,000 customers were Universal Insurance of North America, Gulfstream Property & Casualty, and Southern Fidelity. Over the last couple of years, the insurance industry lost more than $1.6 billion in underwriting in the past year. Insurance companies reach a point where some insurers couldn’t tread water anymore without taking significant actions to reduce their liability.

While some insurance agents reached out to their customers to let them know they were getting dropped, it was the responsibility of the State to send out notifications. With hurricane season approaching, most customers were notified with very little time to find a new policy before the season started. This means many homeowners went without coverage during the storm season.

Even though most Floridians did not lose their insurance coverage, homeowners saw a massive increase in their premium when renewing. The cause behind this, says insurance companies, are the fraudulent claims such as roof claims and lawsuits. This has led the insurance companies to recalculate premiums and raise rates to the point where they are going to collect the cost of a new roof in about three years’ worth of premiums. In addition to raising premium, some insurance carriers have decided to not renew some policies and to only accept new customers with newer home and roofs.

what to do if your insurance rates go up

Your homeowner’s insurance company is required to tell you if your rates increase. If you noticed something has changed on your bill, like an increase in coverage amounts and higher rates, the first thing you should do is call your insurer and discuss your bill with them. They’ll most likely give you a reason and may suggest tangible ways to get your rates lowered as well as any potential discounts you’re missing out on.

Some reasons your insurer may give you for why your rates went up are out of your control, like an increase in natural disasters. But there are several ways you could lower your premiums if they went up.

how to lower our homeowner’s insurance rates

If you’ve noticed your rates have gone up recently and you’re wondering if there’s anything you can do about it, you’re not alone, and yes there is. Following the steps listed below is a good starting point, but you can also call and discuss your rate increases with a licensed representative who can help you better understand your bill and get those rates down.

Look for discount opportunities

When you look at your policy’s declarations page, you’ll notice a discounts section, and if that section is more or less empty, you should look into potential discount opportunities offered by your insurer. Potential discounts you should expect to see offered are:

Multi-policy discount: If you have two or more policies with the same insurer, like home and auto and life insurance, that can potentially save you anywhere from 20% to 30% on premiums, depending on the insurer

Claim-free discount: Some carriers will offer you discounts for not filing claims

Protective devices discounts: If your home is fitted with deadbolts, smoke detectors, fire extinguishers, and fire and burglar alarms that contact law enforcement directly, most insurers will offer you a nice discount

First-time homebuyer discount: Most insurance companies will offer discounts for new homebuyers

Senior citizens discount: If you’re 55 or 60 and older, your insurer may offer up to 10% off your premiums

Long-term policyholder discount: If you’ve been a policyholder with the same insurer for five years or more, it’s common for insurers to offer 10% loyalty discounts

Choose a higher deductible

The lower your policy’s deductible is, the higher your premiums will be, and vice versa. If you’re currently paying a $500 or $1,000 deductible and your rates went up, a good way to get those down is to ask your insurance company about raising your deductible. You only pay your deductible when you file a claim, and if you’re a responsible homeowner who’s never had to file a claim before, then increasing your deductible may be a good option for you.

Disaster-proof your home

If you remodel sections of your home, modernize or winterize your home’s electrical and plumbing, or added storm shutters, storm-resistant shingles, or a disaster-resistant garage door to your home, let your insurance company know — they will likely reward you with lower rates.

Reshop your homeowners’ insurance

You should consider reshopping your home insurance every year to make sure you aren’t missing out on a better deal with a different insurance company. Also, discuss your coverage with a licensed representative to make sure your policy contains all the available discounts and coverage need to keep you safe but also budget friendly.

The IDEA Club

EDWIN GONZALEZ

INTEGRITY INSURANCE

Edwin started as a licensed agent in the insurance industry in 2008 while going to school for his Bachelor’s degree at the University of Central Florida. Edwin is an insurance agent providing solutions for Home, Auto, and Business insurance needs and understand that each customer is unique when it comes to insurance coverage. What he provides is a way to help navigate the insurance industry and provide his my clients with the best value for their dollar, while supplying a superior standard of protection. The companies he represent offer tested, reliable insurance products, excellent customer service and have an outstanding reputation for fast, fair claims service.

Edwin hopes you will take advantage of his industry experience and let him serve you for all your insurance needs. He encourages you to contact him with any questions or concerns you may have.